There is just one thing I hate about start-up company exits (sale or IPO): they can destroy relationships and bring out the worst in some people. In the start-up world, people work for years, often more than a decade, for one big payday, the exit, when their equity stake turns into spendable money, hopefully quite a bit of it. When a large amount of money finally flows, stakeholders often make demands, usually backed by threats, to recut the deal in their favor. People get very angry, relationships are lost, and the exit can even fall apart. Managing this problem is vital.

Companies have ownership structures that are designed to determine who will receive what payments if the company is sold, or who gets what shares if it goes public. These are carefully documented and enforceable in court. When key employees are hired, they receive equity awards (shares and options) that are part of this structure, as are the securities purchased by investors and sometimes granted to strategic partners. These transactions are documented carefully. The board of directors is responsible for administering these agreements. All this amounts to an explicit, detailed, and formal attempt to pre-bake who receives what when the exit finally occurs.

Alas, dividing up the proceeds is rarely straightforward, for two reasons. Over the years circumstances can evolve in ways the original documents did not anticipate. This creates both legal ambiguities (the documents don’t address the actual situation) or legitimate fairness problems that the board of directors needs to address. And, key people have leverage as an exit approaches. The company needs them to put on game faces and sell in the due diligence process. Major shareholders (e.g., founders no longer at the company) need to approve the transaction to allay the buyer’s concern about lawsuits. The buyer or IPO underwriters will want the key employees to pledge continued service to the company, as they are a big part of the value. And some investors have been known to make demands at the goal line, too. The legal ambiguities, fairness problems, leverage enjoyed by key employees/shareholders, and plain old greed can mix together, creating a toxic brew.

I was an investor in and board member of “Sparkle” (made-up name), a start-up company that a major industry player offered to acquire. One of the VPs (“Gus”, also a cypher) had come onboard in the last couple of years and received the standard equity incentive for a VP: about 1% of the company, vested (i.e., doled out) over four years. Hence he would receive only ~0.5% from an immediate exit. He came to the CEO and demanded immediate vesting of his equity. And, he threatened to poison the well during the due diligence process if his demand was not met. There was no legal ambiguity (the option award was well documented) and no fairness issue either: the other VPs had similar equity award percentages and vesting formulas, and they had served much longer: it would be unfair to them if their aggressive colleague received the same value from the exit. But Gus made a naked threat to torpedo a 9-figure acquisition. Regrettably, this kind of thing is pretty common.

Fortunately, the CEO was able to stand Gus down with a minor concession that was tolerable by peers. The CEO is a good manager who had built a good relationship with this somewhat difficult man. I wasn’t in the meeting with Gus, but I helped prepare for it. The case we made went: Gus was probably not important enough to kill the deal, and if he did somehow kill the deal he would have to face his colleagues and the shareholders the next day. If he was found to have lied to the acquirer, there could be lawsuits. The CEO is a calm man with a fatherly personality. Gus saw reason.

These situations are highly frustrating, sometimes painful. Here is how to minimize the pain.

Keep your documentation in good shape, especially documentation of liabilities, securities and equity awards. You’ll be glad you did.

Plan for the exit negotiations. For example, when you structure equity awards to key employees, delay post-exit payout of about half the award until the employee has remained with the buyer for about a year, provided s/he is offered a suitable job. Otherwise acquirers often force sellers to give employees extra incentive comp to stay on. Experienced employees know to expect this kind of deferral: they get that the mission is to build the company and then realize value via sale or IPO, and key man retention is necessary to mission success.

Keep the dialogue and relationship with key employees strong. Festering disputes and insults will erupt at exit time when stakes are much higher.

Pay attention to the buyer’s reputation. Some play it relatively straight and some are crafty folk who like to play games. The buyer’s games, e.g. the details of the key employee retention program, can add fuel to the fire described above. If you have a choice, you might prefer a more straightforward buyer, else be extra sure to have your house in order before entering the M&A process.

As you start the stakeholder negotiation to adjust payouts, make sure you have the key facts well documented and ready to share. People will have varying recollections of key facts and past conversations, recollections usually aligned with their interests. A shared understanding of the facts reduces the scope and impetus for re-negotiation.

Stay on top of the numbers: how much each person will get, how big a difference the disputed points make. In a great exit where everyone gets rich, it’s usually easier to work things out: there’s no hardship and a huge shared interest in closing the exit. The battles are most intense when management and investors have been working for a long time but have to settle for an exit that fails to pay back capital and leaves managers with small reward for long effort. Everyone may feel deep down that they deserve more, and this is the last chance to push for it. Reaching agreement can be very hard.

Listen to arguments about inequities seriously but remember that your job is not to be everyone’s friend. There usually are some situations that need equitable adjustment, for sake of fairness of expediency, but in most cases adhere to the contracts.

Last, do not let emotion take charge. Many stakeholders will quickly go emotional because the stakes are high, they have a lot of themselves invested in the situation, and they may think they can win that way. It’s usually good to listen carefully and show that you feel strongly too, but then you need to bring the temperature down and emphasize facts, standing agreements, the need for fairness on all sides, shared interest in getting the deal closed, and the value of maintaining relationships.

In my experience, most deals get done in the end, very few participants get everything they wanted, and not everyone parts friends. You’ll do better if you are prepared, patient, and cool in moment. Good luck!

First posted @ blogs.forbes.com/toddhixon on May 8, 2018.

After 20 years of early-stage investing, I’m often asked for help with investor presentations. It’s a tough challenge: there is so much you could say in a first pitch, and a limited amount of investor time and attention to work with. If it goes badly, there’s seldom a second chance with that investor.

Start with the fundamentals in mind. Investment decisions are driven by the balance between greed and fear. In a first meeting, you need to accomplish two things. You need to get the investor excited about your opportunity. And you need to make the investor believe you have a good chance of success. The rest can wait.

The investor is mostly trying to decide: “Am I interested?” S/he probably knows the market space fairly well but knows very little about the company. S/he will not be making an investment decision that day. The meeting is about deciding whether or not to put in more time and resources to understand the business better and get to know the principals.

You need to get the investor excited about your opportunity. For venture investors, these factors create excitement:

Your market is huge and accessible,

Your value proposition dramatically satisfies a painful, high-priority need for a buyer with money and decision authority,

Credible third parties judge your product to be much better than alternatives [respected industry leaders are more credible experts than research houses],

You can create strong and sustainable competitive advantage,

You have a way to reach buyers quickly and economically.

Putting this all together: investors look for big value creation opportunities. Most VCs think that at least $1 billion of U.S. market opportunity is needed to move the needle for their fund and justify the risk of early-stage investment. And, they want to see an A-list team signed up to execute and deliver this promise.

You can create excitement and momentum by showing that your business has all or most of these factors working for it. If there are a few gaps, talk briefly about how you will fill them.

Now you need to demonstrate that the risk is less than investors may fear. You do this by showing that:

The business model is working: lighthouse customers on-board, a rising revenue curve, demonstration of value-in-use for buyers, and data that says buyers are using the product, expanding their use, buying again, and recommending it to their friends.

The founders know the market deeply and have valuable relationships: they understand what customers want and how to sell to them, and they have access to key strategic relationships.

The founding team has all the key skill sets.

The founders have a track record of success as entrepreneurs.

The founders are deeply committed and have personal skin in the game.

And, last and most, the founders are very smart, creative, and tenacious business people. Usually it takes a face to face meeting to communicate this.

It can help if there is a successful analog to your business to which you can point. But, VCs know that the greatest innovations have no analogs: before Intel there were no microprocessors; before Facebook no social network …

A couple of “don’ts”: excessive detail in the first pitch (or sent in advance) interferes with creating excitement. Professional VCs and many individuals will not make a decision to invest at the first meeting, but they could make a decision to be excited and start talking up the opportunity, however. A big data dump puts investors in analytical mode, reserving judgment until they process the information. This reduces potential excitement.

It’s usually better to avoid putting valuation and terms on the table. This starts a nerdy negotiation that does not build enthusiasm. And you benefit from hearing what several investors think (i.e., what the market bid price is) before you stake out a position.

And don’t have a weak core team which you try to bolster with long list of part-time executives and advisors, even if their resumes look great. Investors care mainly about the core team and are skeptical that part-timers and advisors will really put shoulders to the wheel.

There are some other bases you need to touch: how your product works, its development status, how much money you want to raise, what major milestones you can reach with that money, how fast you expect to grow and reach break-even and how much total financing you need to launch the business. But keep it brief and stay focused on developing investor enthusiasm and rapport.

Success looks like this. The investor goes back to his/her partners or fellow angels and reports: I’ve found this very interesting opportunity. Here’s why I really like it … [elevator speech]. The entrepreneurs are really impressive, and I’d like you all to meet them: I’ll get that on the calendar ASAP. Meanwhile, I’m going to spend some time and dig into this. We should be prepared to move fast because I suspect that XYZ is talking with these people too …

In the follow up call when the investor asks for a second meeting, listen carefully to learn what objections his/her partners raised, where the investor wants to learn more and where s/he needs more proof. Focus the follow up meetings on these areas. As you do so, you also need to re-enforce the key selling points, fill any gaps so your story works as a whole, and build your relationship with the investor by listening and finding what you have in common.

These observations are drawn from venture capital, but the fundamentals of investment decisions are universal. My fund-raising credo is: energize the greed, calm the fear, and build trust.” Steering by these stars, and with some luck [always needed], you will soon have a new investor and the capital to show the world what you can do.

First posted @ blogs.forbes.com/toddhixon on April 23, 2018.

The world has awakened to the danger in Facebook: it learns a great deal about who its users are as people. Then it enables advertisers and apps on the Facebook platform to take advantage of that knowledge and, in some cases, access the data. That can be a bad thing if, for example, Russian spooks place Facebook ads designed to amp up political polarization and tip a presidential election or the Brexit referendum. It can also be a very good thing when a small business needs to bring a legitimate marketing message to a very specific audience efficiently.

Russia and Cambridge Analytica have created a “#MeToo” moment for Facebook: the media echo-chamber is resonating with reports of deep concerns about privacy expressed by Facebook users, and commentators are speculating that Facebook may need to have its wings trimmed or become a regulated utility. Jealousy spurred by Facebook’s amazing success may be part of the mix, too. Like sexual harassment, concerns about online privacy have been simmering for years, and recent events have triggered a boil-over. Congress has summoned Mark Zuckerberg for a grilling that commentators expect to be arduous. 44 senators attended the first session. Senator John Thune commented: “It’s extraordinary to hold a joint committee hearing. It’s even more extraordinary to have a single CEO testify before nearly half the United States Senate. Then again, Facebook is extraordinary.”

In the midst of this brouhaha, let’s keep our eyes on the fact that 1) Facebook creates enormous value for both users and advertisers, and 2) it’s a unique, young business that has risen very recently to global prominence and hence not had much time to understand what it means to be an important institution and figure out how to play its important role in the information economy, media, and (inevitably) politics.

Facebook is a terrific tool for entrepreneurs, and they will suffer if it is crippled. Consider this example: I work with a company that sells specialized products to consumers. A large part of its revenue comes from three groups of consumers with three distinct psycho/demographic profiles (e.g., age, gender, stage-of-life, preferred activities, and self-image) who are a small percentage of the population and spread across the country. My company offers a strong and simple value proposition: better price and convenience for people with the right profile. Its big marketing challenge is finding the people with these profiles and letting them know what it can offer them.

Conventional media are little help. They mostly serve geographic territories or broad demographic groups and have little ability to target customers based on factors like those above. For example, the audience for Good Morning America, one of the choice advertising platforms on television, is usually described as adults aged 25 to 54, with a tilt to women. This is inefficient advertising if your product appeals to a small percentage of adults. Google is a great resource, but its targeting ability centers on people who have intent to buy specific products. Facebook has unequalled ability to deliver a message to consumers based on tight psycho/demographic factors like those above.

This week Congress and the media are busy weighing how acceptable Facebook’s data and understanding of its members, and its business model which allows advertisers to take advantage of that information, can be. Keep in mind that all marketers need and attempt to target customers (find those most likely to be interested and deliver a message to them), and media companies have always worked to help them do that. Google and Facebook are making waves because they do this better than ever before.

Consumer attitudes towards ad targeting are tricky. Research shows repeatedly that most consumers prefer targeted ads, but many consumers don’t like the fact that their data is used to effect targeting. Many digital ad consumers seem to want the impossible: targeting ads without collection of the data necessary for targeting. Similarly, many TV watchers like the shows they watch and complain about the commercials, but they continue watching. Today technology for on-demand video streaming enables Netflix et al to offer high quality original shows ad-free. But most people continue to watch ad-sponsored TV. Likewise, despite discomfort with ad targeting, billions of people continue using Facebook and Google, because of their unique value.

Successful media is powerful, and power creates danger. Facebook is the next stage in an evolution that began with the invention of the printing press in 15th century Germany. Printing enabled low-cost books and pamphlets, the first form of mass media which, over the next 150 years, changed the political map of Europe by greatly accelerating the spread of ideas. This evolution continued with newspapers, radio, television, and now internet media.

Facebook is also a quintessential Silicon Valley company: brash, focused on growth, moving fast, breaking and fixing things fast. The power of its platform created dangers: loss of control of confidential user data, spreading fake news, exploitation by Russia to sway elections. The current Facebook furor has more to do with these dangers than with targeted ads, which are the core of its business model. Facebook needs to develop rules (probably with government involvement) that preserve the core of its value for users and advertisers while curbing misuse and danger. Zuckerberg openly states that they have not done enough to address the dangers and some form of regulation is acceptable. Other media have faced similar challenges and found a balance between their business models and public interest: newspapers have had centuries to work this out, and even television is now 75 years old.

Facebook leads the next wave of media innovation. It creates danger and great value, particularly for small businesses trying to reach smaller, specific customer groups, and for its billions of users. The Government and Facebook need to learn how to use Facebook’s power wisely, not destroy what is great about it. Let’s not throw this big baby out with the bathwater.

First posted @ blogs.forbes.com/toddhixon on April 11, 2018.

Accounting is a nuisance for many entrepreneurs: a lot of time spent on things that don’t feel like top priorities. However, entrepreneurs should never take their eyes off one financial ball: “Rev Rec” (revenue recognition). It tells you a very important thing: how much money you have to work with, now and in the near future.

The base principals of Rev Rec are simple. 1) You recognize revenue when you have earned the right to receive payment and you have a strong expectation of receiving that payment. 2) You earn the right to receive payment by delivering your value proposition as agreed. 3) You match revenue earned to the costs associated with producing that revenue: i.e., if delivery occurs over several quarters, you recognize revenue each quarter in proportion to delivery of value. This tells you what your profit margin is: how much you have to spend on variable and period costs over the time it takes you to deliver the product that brings in the revenue. That tells you how much free cash you will gain when the job is done. 4) You judge whether the customer will pay: if payment is in doubt, you don’t have revenue.

These principles apply a bit differently in different business models, but the intent is always the same: to determine and report how much money is coming in.

Booking and payment are not the same as revenue. A booking happens when a customer enters an agreement to purchase. At that point your company has not yet earned the right to be paid, and (typically) the customer has not paid. Bookings are a useful leading indicator and you should track them closely, but substantial risk separates bookings from revenue.

Payment can occur before or after Rev Rec. Early payment is great for cash flow, but keep in mind that your company has not delivered yet, and the customer has not yet put your product to use and received value. The contract may say that you get to keep the money if the customer never utilizes your product, but that is low-value revenue: customers who don’t use your product probably won’t buy again and new customers will learn to refuse up-front payment. Late payment is less good, but if the customer is satisfied and a good credit, you can count on the cashflow over time and borrow against it if necessary.

Investors track revenue closely: it’s often the #1 success indicator for a company. When a business takes off, revenue growth happens first, then margin expansion, then positive cash flow. When revenue growth stalls, something is wrong: product/market fit, go-to-market strategy, people not up to the job, etc.

As a general rule, it’s not wise to be aggressive with Rev Rec, even if GAAP (generally accepted accounting principles) permits it. Stuffing your distribution channel with product is an example of aggressive Rev Rec: the channel may buy on terms that technically allow Rev Rec, but an overstuffed channel does not re-order until sell-through occurs, and if financially fragile it may not pay until it collects from end-customers, regardless of what the contract says. Sometimes your distribution channel is inside of your customer: you might be selling seats for a SaaS product to a corporate function in a big company that needs to deploy your seats to operating groups. I’ve seen situations where the corporate function over-buys and then stops buying until it can use what it’s bought. If the channel is stuffed, a recent revenue up-tick does not indicate real momentum. Many companies look through channels and base their Rev Rec on end-user purchase and adoption. That is a gold standard.

Understated Rev Rec is a mistake too: a customer or investor may be lost due to under-selling. Few entrepreneurs have this problem, however, and it’s self-correcting. The company quickly acquires a reputation for beating expectations, and that brings customers and investors in.

Think of Rev Rec (and really all financial reporting) as communication: helping your stakeholders understand what is happening and strengthening your partnership with them by building trust. It’s tempting to push revenue up to build perceived momentum, perhaps ahead of a financing or a big customer proposal. But, if your Rev Rec later falls apart, there is a big price to be paid. Stakeholders will automatically discount future revenue reporting until you re-build credibility, which takes a long time. This taints everything you say, not just revenue. Sometimes this situation creates pressure to exaggerate revenue further to overcome the discount factor, leading to bigger roll-backs and greater stakeholder alienation. In bad cases a death spiral results: investors, employees, and customers lose confidence completely and walk away, or senior management is forced out.

Take two ideas away from this post: you can delegate a lot of accounting tasks, but keep a close eye on Rev Rec. Use it as a tool to keep stakeholders informed as to the health and momentum of the business, building trust and loyalty. With your feet firm on this foundation, you can tackle other challenges with confidence.

First posted @ blogs.forbes.com/toddhixon on March 26, 2018.

Most inventions achieve little or no commercial success. The problem is often a marketing failure: a promising innovation is never brought to customers in a form that they will buy. Inventors need marketing mind-set and skills to get their inventions into the end zone.

Many inventors, particularly technologists, invent because they see a way create a product that has breakthrough properties: it does something faster, better, or cheaper than ever before, or something that has been imagined but not previously realized. Inventors quickly see ways to use their product. For example, as image-forming chips became small and cheap, inventors created digital eye-shades: a pair of dark glasses that form an image on the back of each lens which the eyes see as a single picture. You can put them on and watch a movie from your phone that appears to be on a big screen.

Inventors have great passion. They demonstrate their product to everyone who might be interested. The message is: “This is really cool. If you like watching movies, you will love these digital eye-shades.” They file provisional patent applications (a 2-page description of the invention that the patent office accepts without commitment). They reach out to investors and talk about their product’s breakthrough performance and their “patent”, proposing a multi-million-dollar investment.

Too often this goes nowhere. Most of the time, customers will not buy technical performance alone, even highly technical customers, and investors pass politely: “This is very interesting but it’s just too early for us. We’d love to track you. Please come back when you have orders worth $1 million.” The invention sits on the shelf, or an established company may copy and integrate it into their product line.

The most successful inventors cross this gap by turning themselves into marketers. Their mind-set shifts dramatically. They focus on solving a problem or making life or business better for a valuable group of customers, and they stop talking about the performance and obvious value of their invention. This sounds simplistic, but in practice it’s profound.

The first task is finding a group of customers for whom the invention can make a big positive difference. The difference needs to be big enough that customers will 1) buy and 2) truly adopt the new product: make it part of their lives, buy more, and recommend it to peers. The problem you solve needs to be on the top-three problem/unmet need list for a person who controls enough money to make the purchase. Solving minor problems is no good: they usually don’t make it to the top of the action list.

The potential customer group must be big enough to make your business worth the effort to you and to investors. To raise venture capital, you need a U.S. market opportunity in the $ billion range. (Angel investors may go for less.)

Next, you need to immerse yourself in your customer’s world. Where does the problem you solve fit into their way of doing business or lifestyle? How high is it on their hierarchy of needs? How do they describe their need? Is it part of a bigger problem from their perspective? The customer may be looking for a broader solution of which you provide a part. If so you need to find a partner who can integrate your tech into a solution. Digital eye-shades were developed, and companies were funded, but few customers wanted to buy another piece of gear for the rare situation when they would put on an eye shade and watch a movie in isolation from others, most likely on a long flight. But digital viewers took off in the form of tablets, a broader solution encompassing communications, multi-media and PC-like functions, and less isolating than digital eye-shades.

How does the customer buy this kind of thing, and how do you get on her/his radar? Every market has its specific workings. Studying customers and thinking as they do will point you in the right direction. I find it very useful to just hang out with potential customers: get to know them as people, understand what their big wants and frustrations are, see how they like to do things. Trade shows can be a good opportunity to do this: lots of customers are there and open to talking, potential partners are there too, and you can often find background information on the market. At first, don’t try to sell anything. Just listen.

You want to design your business so that you will be the best at meeting the need you decide to target; otherwise you could get blown away by established competitors once they see what you are doing. Product superiority is one way to do this. Disruptive innovation is a subtler approach: at first, you attack a part of the market that established competitors think is not attractive, then you boot-strap your company into the mainstream. Harvard Business School professor Clay Christensen wrote the book on disruptive innovation. Don’t count on a patent for protection: small companies often have great difficulty enforcing patent rights.

Marketing is a big subject and a career; this is just the skeleton. You can bring marketing expertise onto your team. But your company will be more successful if every important leader learns to think like a customer and feel what they feel.

First posted @ blogs.forbes.com/toddhixon on March 12, 2018.

Amazon together with J.P. Morgan and Berkshire Hathaway (let’s call them the “Triad”) recently announced plans to form a joint venture designed to provide more cost/effective healthcare (“higher employee satisfaction at reasonable cost”) for their 1+ million employees. Although the details are sketchy so far, the announcement drew a large amount of media attention and the stock prices of major healthcare services and products suppliers dipped on the news.

The question on many minds is: can Jeff Bezos with his powerful partners change the U.S. healthcare system, and improve its cost/effectiveness, anywhere near as dramatically as he has changed U.S. retailing, then cloud computing, and now television, the smart home and space transportation? While it’s hard to say what the limits are for a man of such talent, let’s look at the characteristics of the challenge before him.

What are the big levers in healthcare economics? There are three: coordination, clout and behavior.

Coordination refers to the flow of information in the healthcare system, which often breaks down. It is hard for a payer, provider, or individual to assemble and analyze the complete picture of information relevant to the health of one person, or a group of people, so as to draw conclusions, take action or allocate resources in a way that produces the best outcome. Partly this is a technology problem, but many of the barriers to information flow arise from ingrained behavior, regulations, and economic or political incentives. Poor coordination drives higher costs due to repeated tests and wasted time, and it leads to poor patient outcomes.

So, how much of a difference can the Triad make to the cost of healthcare and their employees’ satisfaction with it, and what does this mean for others? What the triad intends to do is vague at this point: “the initial focus of the new company will be on technology solutions that will provide U.S. employees and their families with simplified, high-quality and transparent healthcare at a reasonable cost”.

Bezos speaks of taking out middlemen in the system, like insurers and pharmacy benefit managers (PBMs). Big companies like the Triad already self-insure their healthcare, so taking out insurers matters little. Building a private supply chain for prescription drugs is an intriguing idea: drug company CEOs complain that the pharma supply chain absorbs 40% of drug spending. However, the Triad companies probably spend less than $3 billion on drugs each year, while ExpressScripts, the leading PBM, does about $100 billion of prescription drug business. ExpressScripts has a huge scale advantage purchasing drugs and building the systems needed to process the billions of prescriptions that it handles. If Amazon takes this on, they could develop an attractive service based on their tech and logistics capabilities, but they will need to make huge investments and will probably want to make their service available to other companies to gain scale. That would be good news entrepreneurs.

Communication among providers and the user interfaces for providers and patients are the places where tech solutions can probably make the greatest difference. This is not a green field. Most medical records are electronic now (but in hundreds of systems with dozens of access protocols/data formats). Many small and large companies are working on systems to improve data flow among providers and payers. Some large integrated health systems, like Kaiser Permanente, have a complete picture of a patient’s medical record today. And efforts to improve coordination still face major friction from privacy regulations, doctors’ reluctance to spend time learning new systems and entering data, and the incentive institutions have to hold on to data and use it for competitive advantage, particular in the dawn of the age of artificial intelligence, for which data is the main fuel. Perhaps the Triad can create a medical data superhighway for its employees, however, it’s likely to be a costly slog and benefit mainly the Triad, not other companies.

The patient user interface, on the other hand, has received much less attention and offers significant opportunities. Typical patient portals offered by providers today are the tech equivalent of a 1960’s Dodge Rambler: outdated, underpowered, and just plain ugly. And multi-media communication between patients and providers (internet video, photo + phone, apps, text, etc.) that is tightly coupled to the core care process is a large, under-developed opportunity. Here the Triad can use tech savvy to make big improvements in both cost and employee satisfaction. Triad employees will be the first beneficiaries, but the Triad may be able to accelerate provider adoption of these technologies, and other vendors will pick up on ideas that succeed, much as large and small companies learned from Amazon’s pioneer work in e-commerce. This will bring these benefits to most employers.

Behavior is the conundrum of modern healthcare. It is one of the most powerful levers for both cost reduction and health status improvement. The U.S. has shown the world how to reduce smoking, one of the worst behavior-based health problems. But behavior is not at the top of the healthcare agenda: U.S. companies’ spending for employee wellness is less than 10% of spending for healthcare. This reflects the underlying U.S. health culture in which many people expect to do whatever they wish with their bodies and, when a problem happens, get “fixed” by medical magicians, with the bill paid by a third party. There is also a problem of timeframe: employers and insurers often have employees for a few years, but behavior-induced health problems develop over decades, so investment in behavior change does not have an ROI for them.

Tech and financial services companies and leading companies in other industries are investing more in employee health now. This arises from increased competition for high value employees (e.g., top engineers and data scientists), and probably also enlightened awareness of the link between behavior and health. Google, for example, complements its 3-meals-a-day food benefit with a cloud/mobile system that taps into employees’ medical status (with opt-in), their taste preferences, and the menus of its restaurants to offer healthy eating suggestions at the moment of decision via mobile phone. This approach has proven quite effective in both engaging employees and improving their health on measurable dimensions. Hopefully the Triad will raise the ante for employer investment in and impact on behavior-based health.

Don’t expect that Jeff Bezos and the Triad will revolutionize the U.S. healthcare: it’s too much, even for such a powerful entrepreneur. Do expect that they will push the frontier forward in important specific areas. And look for opportunities to benefit from their innovations and take advantage of the new products and services they will create.

First published @ blogs.forbes.com/toddhixon on February 20, 2018.

We’re a few weeks into 2018, and it’s looking like another crazy year: the government has shut down already; controversy swirls around the Trump presidency; fighting continues in the Middle East; and nuclear tension with North Korea smolders. The national media seems like all-politics, all of the time. What is a sensible view of the outlook for the economy and the opportunities for entrepreneurs? What follows is a synthesis of predictions from commentators I respect.

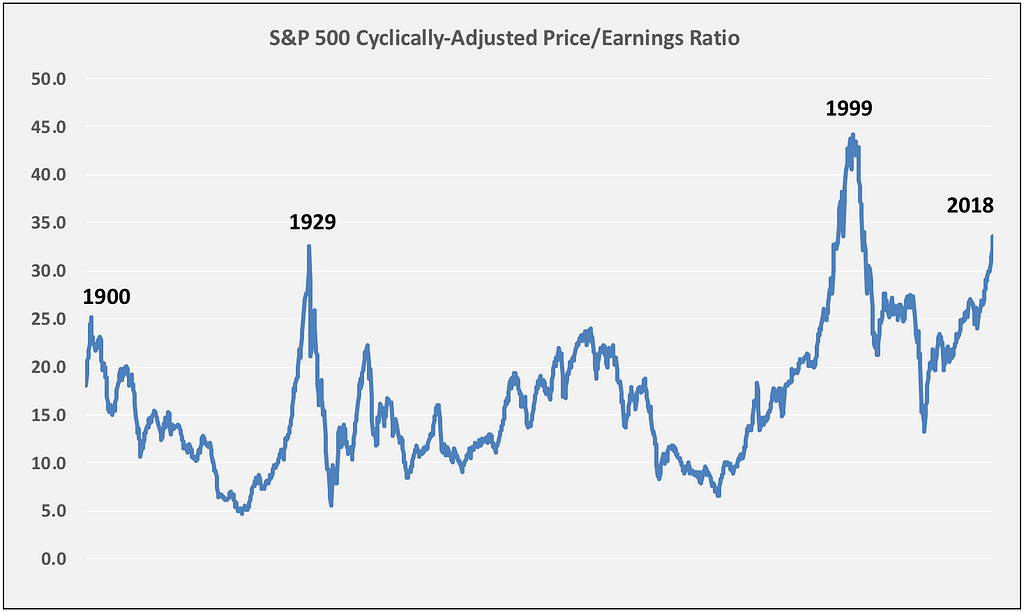

The Economy. How much should we worry about a downturn as the U.S. economic expansion enters its ninth year with the stock market at record high levels? The Economist takes a cautious view of the stock market, noting that U.S. stock valuations (price versus earnings) are at levels not seen in the last century except on the eve of the Great Depression and the Dot-Com Meltdown. It concludes its 2018 outlook with a paraphrase of Dickens’ Micawber: “Something will turn down.”

Data courtesy of Robert Shiller.

Marketplace host Kai Ryssdal is fond of saying “The stock market is not the economy, and the economy is not the stock market.” Economic expansions end due to some combination of demand collapse, central banks raising interest rates sharply, or a general failure of business confidence and financial market liquidity.

On this basis the U.S. economy is positioned for, as the Economist put it, “good-ish [economic] times.” Major economies outside the U.S. are growing, which will create demand for U.S. goods and services, and the 2017 tax act will inject a large slug of demand into the U.S. economy. Europe is finally emerging from a decade-long slump and Macron’s election as President of France has re-energized the European Union. Japan continues to struggle but makes progress. China and India continue to grow much faster than the U.S., Europe, and Japan. Inflation is under control in all these economies. The U.S. economy shows no sign of over-heating: wages are barely rising in real terms and 3–4 million potential workers are still out of the labor force.

The biggest dark cloud in this blue-ish sky is political risk emanating from Korea and the Middle East: if missiles fly of oil supplies are interrupted, the calculus changes. The stock market takes news from these quarters calmly, however, suggesting that investors judge the risks to be modest, or perhaps they can’t really calibrate the risk and see no alternative but to carry on and bet the worst does not happen. This is sensible. Entrepreneurs can carry on building their businesses and pursuing the opportunities that strong U.S. and global economies create.

Disruptive Forces In The Economy. The internet revolution sails on, but the rebels have become the empire. Salesforce.com predicts that Google, Facebook, and Instagram (owned by Facebook) will control 2/3 of global digital advertising revenue in 2019. Facebook recently changed its news feed algorithm, demoting content from corporate sources including web publishers large and small. This put a large dent in hundreds of revenue plans. And the Trump administration has undone Net Neutrality, strengthening the already powerful hands of the telcos and cable MSOs that control most of the U.S. internet access market.

I suspect these companies are approaching a high-water mark, however, caused by their size/complexity and political authorities’ recognition, particularly in Europe, of their enormous power. In the past major tech monopolies have cracked in the vise caused by government pressure on one side and attack from smaller, nimbler companies with new paradigms on the other; government typically responds at about the same time that market forces are beginning to crack the monopoly. IBM, original AT&T, Microsoft (in the PC era), and Intel (in the mobile era) are examples.

For now, entrepreneurs should be prepared to find some toll gates on the road to success. However, these providers have created a mature and powerful infrastructure on top of which entrepreneurs can build additional value. Amazon Web Services, for example, has lowered infrastructure costs for software start-ups by an order of magnitude, notwithstanding it’s quasi-monopoly in cloud infrastructure.

AI applications are almost as diverse as the economy itself. Some are broadly-applicable platforms, such as voice recognition and language translation. Some are very specific problem sets, like diagnosing faults in a jet engine. And some are very big but quite specific markets, like medical diagnosis.

The major tech companies are building AI platforms on which more specific applications can be built. They are also building AI technology for major specific applications, e.g., self-driving cars. Much as Amazon Web Services enabled a generation of software entrepreneurs, the AI platforms have potential to enable a generation of AI entrepreneurs

For example, voice recognition has made “smart speaker” products like Amazon Alexa attractive: Alexa is now usable by most people. Alexa and similar products are driving the market for Internet of Things (IoT) in the home as people use Alexa to control smart lights, smart thermostats, and the like. IoT entrepreneurs are benefitting from Amazon’s AI-driven voice recognition platform. And entrepreneurs are developing strong positions in specialized AI markets. Gamelan Labs offers a service that streamlines a frequent data management problem: comparing two lists with entries that are similar but not identical and determining which are the same and which are unique. This problem arises, for example, when M&A requires companies to merge their customer lists: the same customer may appear in both lists with different profiles. Customers expect to be recognized when they call any part of a company, however, merging large customer databases by hand is slow and expensive.

For large vertical AI applications, like medical diagnosis and population management, large companies have advantages because they control the large datasets needed to train AI systems. But, large healthcare companies need help choosing the best AI technology and developing and applying AI applications. They often want to partner with entrepreneurial companies that can bring these skills and spark change. GNS Healthcare, for example is working with large health plans and providers to help them determine which of their clients (aka “patients”) will benefit most from proactive interventions to head off disease progression.

Crypto-commerce could be the next wave of disruption. Blockchains are a powerful technology that could disrupt a range of information-based businesses including banking. No one has yet built a major blockchain business but many are trying. And blockchain technology enables companies to create and issue money-like tokens such as Bitcoin. Many $ billion worth of these tokens have been purchased, although their long-term utility is yet to be fully determined. For now crypto-commerce is “a sporty game”.

The 2018 outlook for entrepreneurs is positive, despite the torrent of political noise. Some marks by which to steer:

Expect strong demand this year in the U.S. and particularly European countries. Accelerate expansion of your market to Europe and beyond.

Watch out for a dip in the stock market that depresses spending for major consumer purchases, but don’t expect it to depress the economy as a whole.

Respect the power of the major web companies and the telcos. For now, they are having their way and will be able to price aggressively and make dramatic decisions in their own interest. Don’t base your business model on policies they can change overnight.

Think through the impact of AI on your business in two dimensions. Dimension 1 is the potential to create value, especially for customers. Dimension 2 is the relative cost effectiveness different players enjoy creating that AI value: you, your competitors, and your technology and platform providers. Work out how important AI will be in your market and how to assemble the resources (in-house, partners, suppliers) needed to deploy it in the most cost/effective way.

Here’s to prosperity and growth in 2018!

First posted @ blogs.forbes.com/toddhixon on January 26, 2018.

Year end is the time when we wonder what to expect next year. 2018 brings unusual uncertainty: will the unprecedented longevity of the bull market continue with the Fed raising rates? What effect will the speed-dating tax “reform” have on the economy? And what will happen to the cost and quality of our healthcare as the Republicans strip down Obamacare while the chronic disease epidemic and a technology revolution driven by genetics and AI roll on?

Steve Forbes kicks off the annual healthcare summit.

The annual December Forbes Healthcare Summit is a unique gathering of high-level leaders and technologists: for example, five CEOs of major pharma companies participated in the final panel. What follows is a summary of key insights from the conference from an entrepreneur’s perspective.

Multiple speakers warned that the percentage of the U.S. economy devoted to healthcare will continue to rise and become unbearable. This is driven by increasing prevalence of lifestyle diseases (diabetes, heart disease, pulmonary diseases, many cancers) which drive over 80% of healthcare cost*. Many chronically ill people are in the workforce and hence employers are concerned about their health and healthcare cost. Longer lifespans are a second factor driving higher healthcare cost, with the main burden falling on government and then indirectly on employers/employees via taxes.

On the technology front, Vast Narasimhan, the incoming Novartis CEO, laid it out: “Biology is now tractable for many diseases.” Two families told stories of a mother and son entering the CAR T-cell therapy trials as a last resort with months to live, and emerging with no detectable cancer. Many of the earliest patients have remained cancer free for several years. CAR T-cell therapy is based on removing immune system cells from the patient, modifying their genome to circumvent the cancer’s natural defenses, and inserting the modified immune cells into the body. It is expensive because the immune cell modification must be performed specifically for each patient. But it works for a large percentage of patients and shows promise of long-lasting or permanent cure. This is the latest and most dramatic of a series of new drugs discovered in recent years with these factors in common: they are based on genetic and biochemical science; they are very effective for limited groups of patients selected on the basis of genetic characteristics and/or protein expression; they offer long term relief or cure in many cases; and their cost ranges from $50,000 to as much as $500,000 per patient.

Advances in artificial intelligence applications for healthcare help payers predict more accurately which patients will benefit from which treatments/interventions. This makes the silver (or platinum) bullets more accurate but does not reduce their cost. AI promises to reduce costs by automating professional work and increasing accuracy in specific areas of medicine such as pathology, radiology, dermatology, and diagnosis generally.

Critics of the pharmaceutical industry observed that drugs have been one of the main drivers of healthcare cost increases in recent years, mainly due to the introduction of new very-high-cost therapies and in some cases aggressive price increases for established drugs (e.g., epi pens). The pharma CEOs responded that they are innovating powerful therapies that cure or control fatal diseases; the lifetime savings resulting from a cure justify a steep one-time price; patients benefit tremendously from the 90% of U.S. prescriptions that are relatively cheap generic drugs previously invented by pharma companies; pharma manufacturers receive only 60% of drug spending because the supply chain swallows 40% of the U.S. drug dollar and drives most of the overall increase in drug costs; and rewards for innovation need to be powerful to keep cures coming. From all this it’s clear that high-cost therapies will continue to arrive and present big cost challenges to plan sponsors and employees.

What does all this mean for entrepreneurs? Ultra-high-cost therapies mean that employees need health insurance more than ever. And options other than employer sponsored insurance are fewer and more expensive with an uncertain future. The Trump administration and Congressional Republicans continue to weaken the provisions of Obamacare that underpin universal healthcare: e.g., Medicaid expansion, the individual mandate, co-pay subsidies for the poorest exchange participants. This has driven big premium increases and reduced the number of products available for individuals to buy on the exchanges. Costs for employer sponsored plans are reasonably under control, partly because the well established trend to increased employee skin in the game has demonstrated success controlling costs. This is an opportunity for employers: if you can offer a good health plan, it is a powerful recruiting/retention tool.

New approaches to the drug benefit portion of health plans are another opportunity. The pharma CEOs point out that the middlemen are getting too much of the drug dollar and absorbing manufacturer coupons and rebates that are intended to help patients with insufficient insurance benefits gain access to high cost drugs. This is an arcane space where professional help is needed. It appears that new approaches to pharmacy benefits emphasizing mail order pharmacies and coupon targeting programs can drive lower costs.

Diane Holder, CEO of UPMC’s health plan, reminded us that behavior change is the most powerful lever for health cost reduction, and mobile technologies offer new and effective behavior change tools. Elimination of poor diet, inactivity, and smoking would reduce major heart diseases, stroke, and diabetes by 80% and cancer 40%. About one-third of the total benefit comes from smoking cessation alone. Effective approaches to behavior change based on smart phone technology and coaching of both physicians and patients have been demonstrated. As Ms. Holder put it, “We know what to do, we just don’t use what we know. A smartphone makes better choices more likely for many.” Behavior change programs enable employers to both control costs and improve employee health, particularly for long-term employees.

Next year will be a challenge in health care; that should not be a surprise. But opportunity beckons as well. Doctors have new weapons and are able to use them more precisely; employers and health plans can use AI to target interventions and new drug contracting approaches to control costs; and behavioral change, the mother of all therapies, is gaining traction with tools built on mobile devices.

*All the statistics I quote pertain to the U.S. healthcare.

First posted @ blogs.forbes.com/toddhixon on December 20, 2017.

Harvey Weinstein: 80 women have accused him of sexual harassment.

Sexual harassment has been recognized as a major problem, and accused offenders are falling in a range of industries. At long last victims are receiving a hearing and justice. However, a lasting solution will not occur until reconciliation is achieved.

In the past year Harvey Weinstein and Bill O’Reilly in Media, Al Franken and Roy Moore in Politics, several prominent journalists and venture capitalists, and many others have been accused of sexual harassment, and in many cases forced to step down from positions of power. Impressive numbers of women are tweeting #MeToo. The energy that has been released is scary. Listening to Marketplace Tech host Molly Wood talk about harassment of women in Silicon Valley, I am struck by the seething anger they feel.

A picture emerges of powerful men using their positions to force their attention on women, and, much less often, powerful women doing the same to men. This behavior is widespread and has been tolerated in the shadows for decades. Now institutions are responding quickly with investigations and sanctions, and in many cases pushing the accused offender out. Victims see that they can get a hearing and are stepping forward. We seem to have crossed a cultural watershed: harassment is no longer tolerated and perpetrators will be sanctioned.

The next few years will be busy with hearing a backlog of complaints and taking action. This could go quite far. Ellen Pao, a venture investor who departed from and then sued Kleiner Perkins (a top venture capital firm), and whom some regard as the standard bearer for women abused by the venture establishment, argues that a “total reset” of the venture capital industry is needed*.

Amidst all of this conflict, our paramount goal should be reconciliation. Reconciliation requires four steps: political re-balancing, bringing the facts to light, justice for victims and accused people, and building the foundation to move ahead.

South Africa’s Truth and Reconciliation commission provides an illuminating example of how reconciliation can work. It addressed a very tough problem: two centuries of racial discrimination, exploitation, and violent repression. Political re-balancing enabled change: it occurred when South Africa held elections with a broad-based franchise in 1994. The Truth & Reconciliation commission was created in 1995 to drive reconciliation. In a public process, it interviewed victims, recommended reforms and restitution, granted amnesty in some cases and left most for prosecutors. Its work addressed both individual cases and the structural, economic, social, and institutional environment of the Apartheid system. While imperfect, its results are widely admired.

For sexual harassment, political re-balancing is occurring now and seems to have reached a critical momentum. Facts are coming to light as victims step forward and institutions investigate.

Today justice is highly challenged in the sexual harassment arena. Objective evidence about events that occur in private is often scarce. Victims have long felt ignored with good reason. Now the pendulum is swinging against the accused, who often feel they have few rights. Once they are under suspicion, colleagues see them as a big liability: people have been pressured to resign based on rumors alone, before any accuser steps forward or the evidence is examined. Justice is a learning process: companies and courts need to learn how to handle harassment cases well. Reconciliation depends on a better standard of justice for accusers and accused alike. That will require some patience on all sides.

In the venture capital industry, the NVCA (National Venture Capital Association) has moved strongly to define values and standards designed to proscribe harassment and create a framework for fair treatment of diverse professionals and entrepreneurs, specifically including women. This is real only when people walk the talk. It is ultimately up to the leaders of the very private and powerful firms that dominate the industry to drive and cement change.

Establishing new norms and changing behavior takes time, commitment, effort, and tenacity. It is probably most difficult in arenas where the stakes are highest, like tech, finance, media, and politics. But it will happen better and sooner if we approach the task with a philosophy of reconciliation.

Notes: *From the November 15, 2017 episode of the Marketplace Tech podcast.

First posted @ blogs.forbes.com/toddhixon on November 29, 2017.

Almost every start-up has near-death experiences: times when the business is not delivering, money is short, and employees are wavering. Entrepreneurs often call on investors to give them sea room in which to fix problems and rebuild momentum. Great leaders use the tools described below to rebuild investor confidence and win another chance to succeed.

These “moments of truth” test investors’ confidence in the business, its leadership, and their own judgment. Investors’ decisions are based on a combination of logic and emotion. They will look at the company’s data carefully and re-examine the investment case: is the market developing, do customers value our product as much as expected, has another company taken the lead, can a big win still happen?

At the same time they will experience an up-welling of feelings that have decisive impact. When I’ve been in this situation, here is how I have felt:

Frustrated because promised results have not been achieved, for the nth time,

Blind-sided and embarrassed if I just learned that the state of the business is much worse than I knew, and much worse than I told my partners,

Let down and angry if someone I trusted has been hiding the severity of the problem or is failing to take responsibility,

Disillusioned that the vision in which I have long believed seems lost,

Foolish, because it now looks like I should have stopped supporting this business a while back, and I know that supporting failing businesses too long is a mistake for which investors are often criticized, and

At the same time, hopeful that a way to fix the business can be found, because failure will hurt the employees; writing off all the money, faith, and relationships tied up in this investment will be very painful; and saving them will be a great relief.

Handling bad news and failure separates great leaders from others. I have watched many entrepreneurs do this very well over the years. Each leader has his or her own style, however, they employ most or all of the following strategies.

Get all the bad news on the table up-front. Partly this is about managing feelings: you want your listeners to get through the depression caused by bad news, and then build their enthusiasm back up. And you need to reestablish credibility by revealing everything your stakeholders need and want to know. Hiding problems at this stage is toxic: as they say in DC, the consequences of the cover-up are always worse than the offense itself. So take the trash out, and then get to work solving problems.

Take your share of the blame, and don’t go after people, even if they deserve it. No one is blameless in a bad situation. If you focus on blaming others it will look like you are trying to hide your own mistakes. This “control the narrative” strategy may work in politics, but it seldom works with a sophisticated business audience.

Think deeply about what caused the problem, and what change can fix it. Your audience has lost faith in yesterday’s strategy. To buy back in, they need to understand why the company will be more successful going forward. That requires a new approach based on facts and well-reasoned plans.

Make believable projections. Investors know they have lost ground from their prior expectations. Lay out a path to a good outcome that stands up to scrutiny. Include some measurable milestones in the near future, so investors can feel they are “putting down money to see another card.” Lofty promises don’t work in these situations; you probably got where you are by over-promising. Reestablishing credibility is job one.

Display competence, confidence, and determination to succeed. Investors need to see how deeply you understand how the business works, where it is going, what needs to happen, and how to get things done. More important, you need to show you believe your turnaround strategy will work and you are committed and determined to push through to success. Speak calmly about the problems: a measured, confident tone is remarkably effective making problems seem manageable.

Show that you have personal skin in the game. When they put more money into a troubled company, investors feel they are putting their flesh on the chopping block. They will have more confidence if you do so too. This can take many forms. Saying you are investing the “opportunity cost of your time” is not very effective: who knows what that really is, and if you are so great, why are the results not better? Actually writing a check is a powerful way to build investor confidence.

Listen and be reasonable, reminding your investors that you’re a good person to work with. People invest in people, specifically people they like and trust. Your investors need to believe in you as much as in the business.

Sell the upside with quiet passion. This is not the time for a jazzy sales pitch. It’s the time to remind investors that the business is bloody but unbowed, and can deliver a version of the vision and pay-off that led them to invest before. Having rebuilt a foundation of confidence, you can put their eyes back on the prize.

At the core, maintaining investor support is about rebuilding your relationship with investors. If the facts of the business situation are too dire, that may not be enough. But most often investors are making a judgment call. If you manage the crisis by building the right relationship with them, there’s a good chance the call will go in your favor.

First posted @ blogs.forbes.com/toddhixon on November 10, 2017.